Florentine Apartments

Multifmaily

The Florentine Apartments project by VonFinch represents a value-add multifamily investment in Omaha, Nebraska. This 174-unit property was acquired at a significant discount to market value, providing built-in equity at purchase. The investment strategy includes unit renovations, rent optimization, and operational efficiencies to deliver strong returns over a 5-year hold period.

Investing Simplified - Deal Summary

(See Key Terms tab above for explanations of words in bold & italics)

This is a syndicated value-add investment opportunity in which the sponsor acquires a single multifamily property requiring updates and renovations to reach its full potential. Syndications involve a sponsor raising investor (LP) equity to purchase a specific asset, offering investors more clarity and control through insight into the individual property being purchased. Unlike funds that hold multiple properties and seek additionally diversification through multiple assets, syndications focus on one property. Multifamily investments inherently offer diversification due to their multiple tenants, reducing risk and providing stable revenue streams, mking them among the favored syndication investments from a risk prospective. While funds create additional diversification through various assets, it's unlikely every asset will be a standout performer, thus syndications can have higher upside when chosen correctly not being dulled by the law of averages.

The business plan involves modernizing the property, updating individual units, and improving amenities to increase rents to market levels. This raises the net operating income (NOI), directly enhancing the property’s value. Located in Omaha, Nebraska, the property benefits from low vacancy rates, strong demand, and a steady rental base. Current rents are below market averages, making it ideal for this value-add strategy.

Multifamily properties are regarded as stable assets due to their tenant diversification, which minimizes the risk of significant income loss. While competition and compressed cap rates can make securing steep discounts challenging, multifamily investments remain in demand for their stability and reliable returns. In this investment, the sponsor projects a 1.8 to 2.0 times equity multiple, which is considered strong for a value-add strategy.

Investors should note that all projections are estimates based on current market conditions, comparable sales, and the execution of the business plan. Risks include overestimating returns or sale price, and projections depend on assumptions such as successful renovations, rent increases, and market performance. Reviewing these factors is critical, and the AltSpot committee evaluates these assumptions thoroughly.

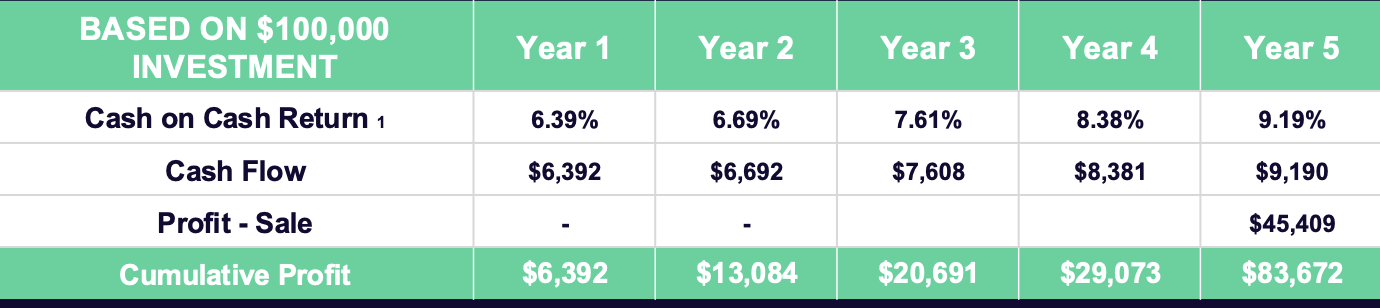

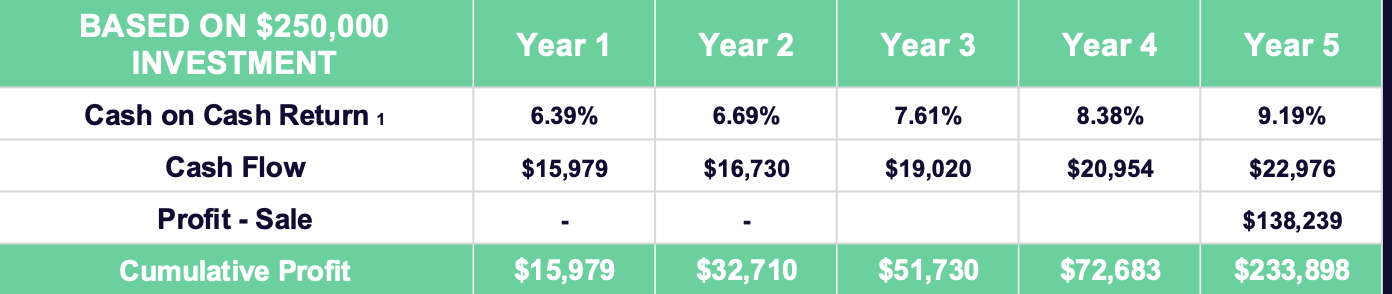

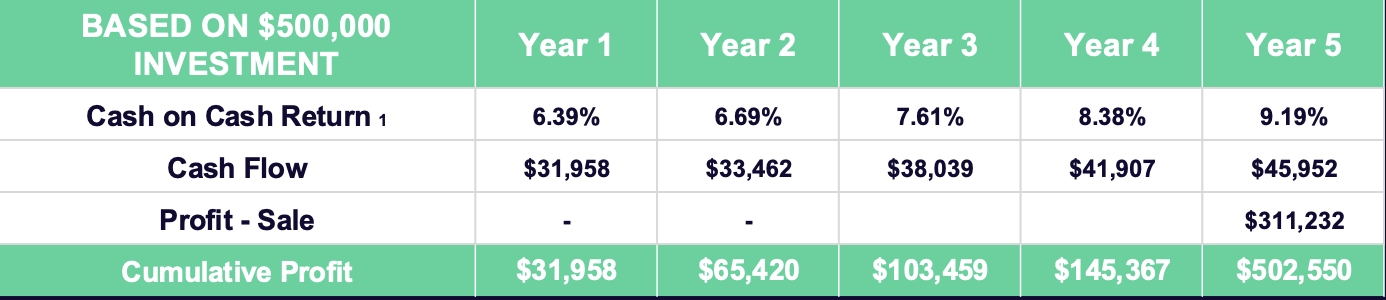

The sponsor, VonFinch, has a proven track record of meeting or exceeding exit projections, providing confidence in their ability to execute. For this property, projected cash-on-cash returns start at 6.3% in the first year and increase steadily, reaching over 9% by year five as renovations are completed and rents adjusted. While value-add deals are not suited for investors seeking immediate high dividends, they offer long-term potential for income growth and property appreciation.

Projected Returns:

In this investment investors ( or limited partners) will be investing in the common equity position of the capital stack. Much like purchasing public common equity shares on the stock market. Common equity investments generally reciveve the highest upside but are the least risk adverse within the capital stack, as debt, subordinate debt, and preferred equity in a traditional capital stack must legally be paid first. It is worth noting however that LP's will be paid before the sponsor ( who is last to be paid in a liquidity event, like a refinance or sale of the asset.

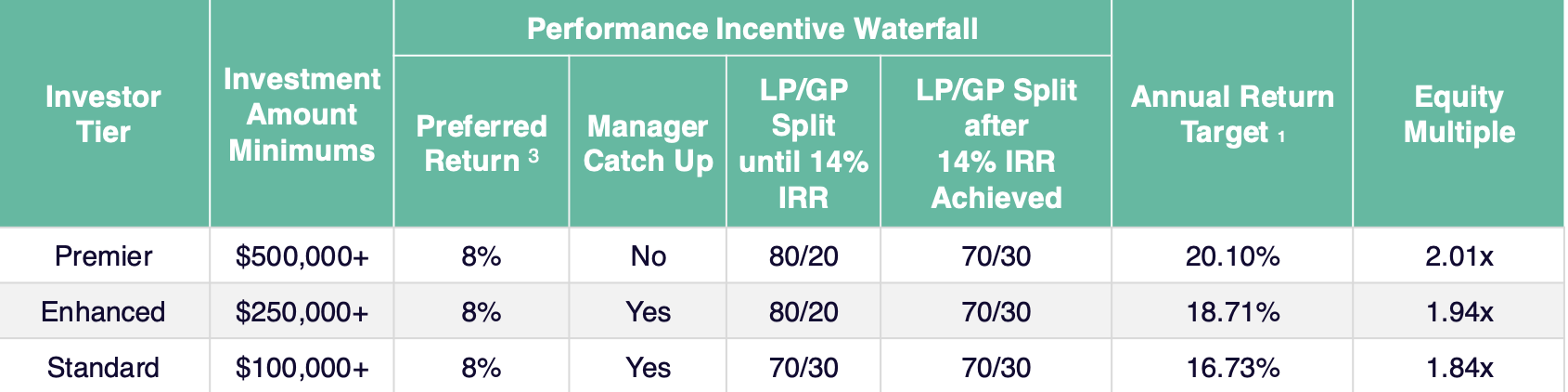

This syndication incentives larger check writers by establishing 3 tiers of investment. Each with their own structure giving bonus incentives via the profit splits and manager catchup.

Note: Its important to not confuse "preferred return" as a cash on cash or dividend return. see Key Terms below for more information.

Investment Tiers

Return Projections by Tier:

100K Investment | 8% preferred return | 70/30 split | *Subject to manager Catch-Up

$250K Investment | 8% preferred return | 80/20 split | *Subject to manager catchup

$500k Investment | 8% preferred return | 80/20 split | * Not Subject to manager catchup

Investing Simplified - Key Terms

- Syndication: A syndication is when a sponsor gathers money from investors to buy one specific property, instead of putting money into a fund that owns multiple properties. With syndications, investors have a clearer view of the exact property they are investing in. While syndications may carry more risk since there’s no diversification like in a fund, they often have the potential for higher returns because funds spread out the earnings across different properties, which can lower the total return.

- Sponsor - The individual who is the managing member of a real estate project or fund. Typically holds "GP" shares getting paid very last behind limited partner shares in the capital stack.

- Manager Catch-Up - is when the sponsor (the manager) gets a bigger share of the profits after the investors have received their preferred return. It’s like the sponsor "catching up" on their share of the profits as a reward for making the deal successful. Once the catch-up is complete, the profits are usually split based on the agreed terms between the sponsor and the investors.

- Preffered Return: A preferred return is the percentage of return LP Investors must reach before the indicated sponsor split takes place. In a deal in which the preferred return is 8% and the "waterfall" ( or split) is 80/20. this means the investors must be paid 8% THEN the remaining funds are split 80/20 between investors and sponsors. i.e you invest $100k at an 8% preferred return with an 80/20 waterfall for one year. At the deal level your 100k basis doubles to 200K. The "waterfall" or split between the LP and the sponsor would look like this. 8% or $8,000 in preferred return would be returned to you first NOT subject to the 80/20 split. There would be $92,000 in profit remaining. $92,000 will then be split 80/20. Investor share being $73,600 Sponsor share being $18,400. Thus the total investor return would be 100K orginal basis + $8,000 preferred return + $73,600 on their share of the split = $181,600

- Dividend: A dividend is the actual cash payment distributed to investors typical on a regal schedule.

- Cash on Cash: return measures the percentage of the investor’s cash investment that they receive back in dividend distributions during a specific period, usually annually

- Hurdle Rate : is the maximum return percentage at which the waterfall split changes. For example, in a deal with an 80/20 split and a 14% IRR hurdle to 50/50, investors will receive an 80/20 split until their total return surpasses 14%. Any remaining funds above this threshold will be split 50/50 between the sponsors and the limited partners (LPs).

- Common Equity: ownership stake help by Limited Partner investors. Common Equity typically get paid after debts and preferred equity are satisfied, meaning common equity carries more risk but also has the potential for higher returns if the property performs well.

- Limited Partner: an LP or investor in a deal that holds common equity shares but has no day to day management or responsibility.

Built-in Equity from Day One:

- Purchased at $65,000 per unit, far below market comps of $90,000–$109,000/unit

- Total project cost, including renovations and working capital, is $14.2M, ensuring cost efficiency and upside potential.

Value-Add Strategy for Growth:

- Planned renovations and upgrades target $147–$282 rent increases per unit, aligning rents with market rates.

- Additional income streams from utility-bill-backs and resident fees further boost revenue.

- Projected 24% reduction in operating expenses enhances profitability.

Market Fundamentals Support Stability:

- Omaha Market Strength

- 3.1% unemployment and steady rent growth highlight economic stability.

- $10.8B in new developments drive growth and job creation.

- The market maintains a strong occupancy rate of 94.4%, with a corresponding vacancy rate of 5.6% as of Q4 2024

- Mid-market rents attract tenants priced out of luxury units, ensuring resilience during downturns.

Flexible Investment Tiers Reward Larger Commitments:

- Tiered structure allows higher returns for larger investments:

- Premier Tier ($500K+): 20.1% IRR, 2.0x equity multiple.

- Enhanced Tier ($250K+): 18.7% IRR, 1.94x equity multiple.

- Standard Tier ($100K+): 16.7% IRR, 1.84x equity multiple.

Execution Risks

Renovations must be completed on time to achieve targeted rent increases and stabilize operations. Delays could impact cash flow projections and investor returns.

Geographic Concentration

The focus on Omaha leaves the project vulnerable to local economic fluctuations, although the market fundamentals are currently strong.

Inherent Value Add Risks

Value add projects require singificant management, and are subject to price variation.

This syndication suits investors aiming for solid, risk-mitigated returns around a proven manager. It becomes particularly attractive for those able to invest at higher tiers of $250,000 to $500,000. Overall, it represents a fundamentally sound multifamily deal that could make a strong addition to many investment portfolios.